Few aspects of running a business in Singapore generate as many questions as CPF contributions on bonus payments. From Annual Wage Supplements (AWS) to performance bonuses and ad-hoc rewards, determining the correct CPF treatment can challenge even experienced HR professionals.

This guide walks through the essentials of bonus-related CPF contributions for Singapore employers in 2025, explaining not just the what, but the why and how—with practical examples and common pitfalls to avoid.

Understanding Bonus CPF Contributions: The Basics

CPF Contribution Basics SG

Challenge observed:

Lim, a director at a local trading company, approved year-end bonuses for his 18 employees. He instructed his finance officer to apply CPF contributions only to bonuses that exceeded $2,000, believing there was a minimum threshold. When MOM conducted a routine audit, they discovered significant CPF underpayment, resulting in backpayments plus penalties.

Regular monthly commissions (these are Ordinary Wages)

Transport allowances (exempt from CPF)

Retrenchment benefits exceeding certain thresholds

Non-monetary rewards (gift cards, prizes, etc.)

Genuine reimbursements of business expenses

Important practice tip: When determining if a payment requires CPF contributions, focus on its nature rather than what it's called. Many employers mistakenly exempt payments from CPF by labeling them as "allowances" when they are actually forms of remuneration.

The Additional Wage Ceiling: How Much Bonus is Subject to CPF?

The most crucial concept for bonus CPF calculations is the Additional Wage Ceiling (AWC).

Challenge observed:

Sarah, HR manager at a local SME, calculated CPF on her employees' annual bonuses based only on the monthly salary cap of $6,000. For a senior employee earning $8,000 monthly who received a $20,000 year-end bonus, she applied CPF only to $6,000 of the bonus. This created a significant CPF shortfall that was discovered during their year-end audit.

Key insights:

The Additional Wage Ceiling works differently from the monthly salary ceiling:

AWC = $102,000 - Ordinary Wages subject to CPF in the year

Each employee has their own unique AWC based on their annual ordinary wages

The AWC can range from $0 to $102,000 depending on the employee's regular salary

Once an employee exceeds the AWC, further bonuses that year are not subject to CPF

Practical solution:

Calculate each employee's Additional Wage Ceiling using this formula:

AWC = $102,000 - (Total Ordinary Wages subject to CPF from January to December)

Example:

Employee with monthly salary of $5,000 ($60,000 annually)

AWC = $102,000 - $60,000 = $42,000

This employee's bonuses are subject to CPF up to $42,000 for the calendar year

Practical Calculation Examples for Different Scenarios

Scenario 1: Mid-Year Bonus

For bonuses paid partway through the year, you need to project the employee's Ordinary Wages for the full year.

Q4: Cumulative $34,000, but only $30,000 subject to CPF(Final $4,000 exceeds AWC and is CPF-exempt)

Scenario 3: Employee with Variable Income

For employees with variable monthly income, the calculation requires careful tracking.

Example:

Real estate agent with monthly commissions varying from $3,000-$10,000

Annual bonus of $20,000 paid in December

Actual Ordinary Wages from Jan-Nov totaling $65,000 (all subject to CPF)

December commission estimated at $7,000

Calculation steps:

Project final month: $65,000 + $7,000 = $72,000 total Ordinary Wages

AWC: $102,000 - $72,000 = $30,000

Bonus CPF contribution on $20,000 (all within AWC)

Special Situations and Common Pitfalls

Challenge observed:

Jason, owner of a small design firm, believed that CPF contributions weren't required for performance bonuses paid to employees over 55 years old since they have reduced CPF contribution rates. This misunderstanding led to incorrect contributions for his senior employees.

Key insights:

Several special situations require particular attention:

Age-based CPF rates apply equally to bonuses and ordinary wages

Bonuses paid in the first year of employment have special calculation methods

Foreign employees who become Singapore Permanent Residents mid-year have pro-rated calculations

Director fees require CPF regardless of when they're approved or paid (with specific computation methods)

Practical solutions:

For Employees Above 55

Apply the age-appropriate CPF contribution rates to the bonus amount:

Example:

Employee aged 60, earning $5,000 monthly

Receiving $10,000 year-end bonus

AWC calculation remains the same

Apply reduced contribution rates based on age band (e.g., 26% total for ages 55-60 instead of 37% for those under 55)

For New Employees

For employees who haven't worked a full year:

Example:

Employee joined in September 2025 at $4,000 monthly

Receiving $5,000 year-end bonus in December

Calculation steps:

Actual Ordinary Wages: $4,000 × 4 months = $16,000

AWC: $102,000 - $16,000 = $86,000

Bonus CPF contribution on $5,000 (well within AWC)

For Director's Fees

Director's fees are always subject to CPF if the director is a Singapore Citizen or PR:

Example:

Director's fees of $50,000 approved at AGM in April 2025

Calculate AWC based on the director's other ordinary wages

Apply appropriate CPF rates based on the director's age

Note that directors over 55 still receive CPF on fees, just at reduced rates

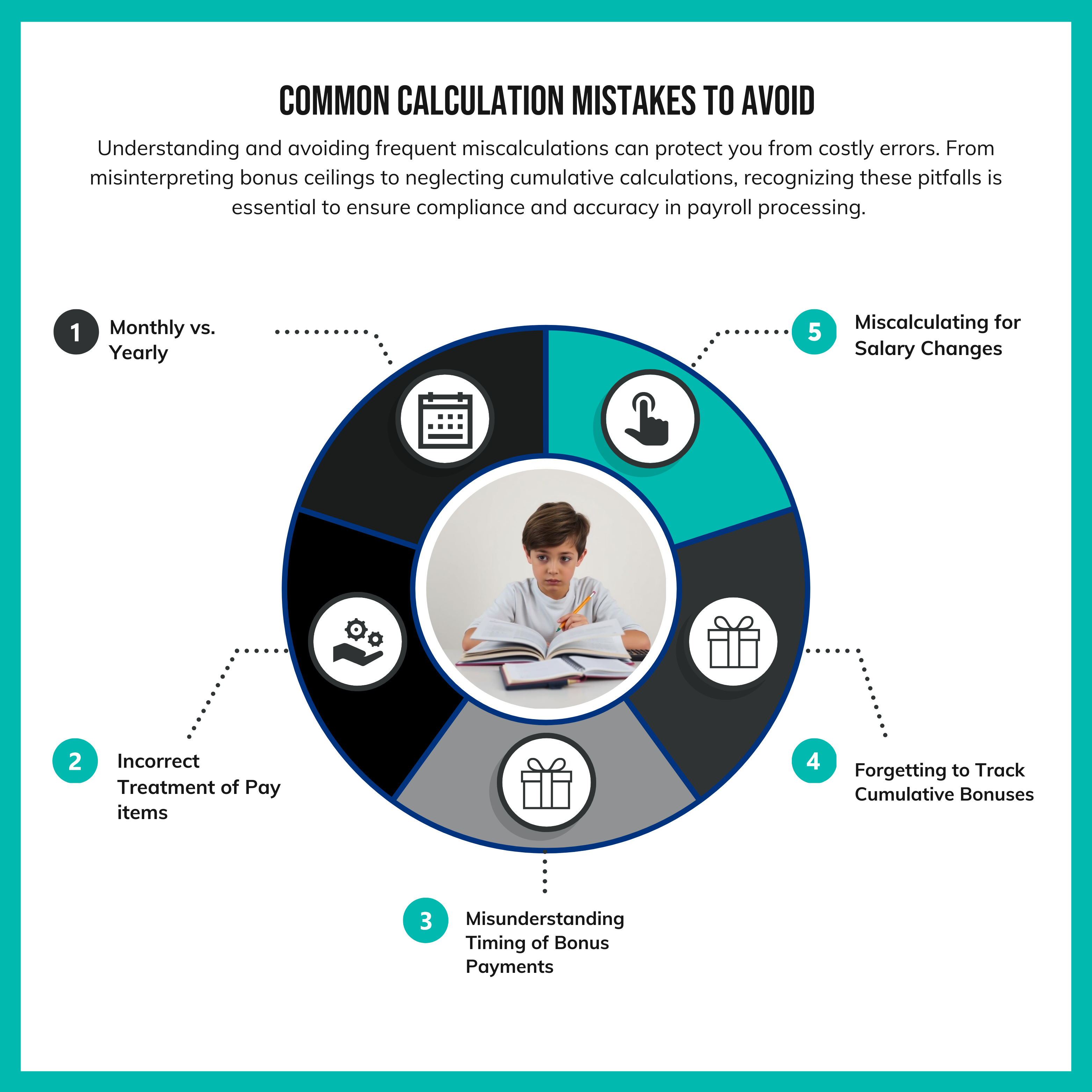

Common Calculation Mistakes to Avoid

CPF calculation mistakes

1. Confusing Monthly vs. Annual Ceilings

Common error: Applying the $6,000 monthly ceiling to bonus paymentsCorrect approach: Use the Additional Wage Ceiling (up to $102,000 - Ordinary Wages)

2. Incorrect Treatment of Allowances and Ad-hoc Payments

Common error: Assuming all allowances are exempt from CPFCorrect approach: Only genuine reimbursements and specified allowances (e.g., transport within limits) are exempt

3. Misunderstanding Timing of Bonus Payments

Common error: Applying different treatment to bonuses paid in January vs. DecemberCorrect approach: The calendar year of payment determines which year's AWC applies

4. Forgetting to Track Cumulative Bonuses

Common error: Calculating each bonus in isolationCorrect approach: Track cumulative Additional Wages against the AWC for the year

5. Miscalculating for Salary Changes

Common error: Not recalculating AWC when an employee receives a significant raiseCorrect approach: For future bonuses after a salary change, recalculate AWC based on new projected annual Ordinary Wages

Practical Implementation for Payroll Systems

Challenge observed:

Mei Ling, office manager at a local accounting firm, manually calculated CPF for each bonus payment, creating significant administrative work and increasing error risk. When auditing the previous year's contributions, she discovered several calculation errors that required correction and backpayment.

Submit CPF contributions by the 14th of the following month

Ensure payment reaches CPF Board by the 14th to avoid late payment penalties

Maintain records of wage and CPF calculations for at least 3 years

Be prepared to provide bonus justification documentation during CPF audits

Late payment penalties:

Interest at 1.5% per month (minimum $5)

Potential composition fines for repeated or severe non-compliance

2025 CPF Updates Affecting Bonus Contributions

Recent and upcoming changes affecting bonus CPF calculations:

Annual ceiling for Ordinary Wages remains at $72,000 for 2025

Additional Wage Ceiling remains at $102,000 - Ordinary Wages for 2025

CPF contribution rates for employees aged 55-60 increased to 28% (employer: 14%, employee: 14%)

CPF contribution rates for employees aged 60-65 increased to 18.5% (employer: 10%, employee: 8.5%)

(Source: CPF Board Employer Update Circular, November 2024)

Conclusion: Getting Bonus CPF Right

Calculating CPF contributions for bonuses may seem complex, but the underlying principles are straightforward once understood. By mastering the Additional Wage Ceiling concept and implementing systematic calculation approaches, Singapore employers can ensure compliance while accurately managing their CPF obligations.

Remember these key principles:

All bonuses are subject to CPF up to the Additional Wage Ceiling

Each employee has a unique AWC based on their annual Ordinary Wages

Tracking cumulative Additional Wages is essential for multiple bonuses

Age-based CPF rates apply equally to bonuses and regular wages

By applying these principles consistently, you'll avoid costly errors and ensure your bonus payments remain compliant with Singapore's CPF requirements.

For assistance with CPF calculations or implementing payroll best practices for your organization, contact Kelick's HR Compliance specialists.

This guide provides general information about CPF calculations for bonus payments in Singapore. While we strive for accuracy, CPF regulations may change. Organizations should verify current requirements with the CPF Board when making decisions.

.png)